The clearest read on construction at midyear comes from the companies getting hired to do the work, and their outlooks point in two different directions. Backlogs are growing, and contractors feel good about their own books. But leading economic indicators signal concern. Nearly every panel expects higher input costs heading into year-end.

Why Contractors Remain Cautious

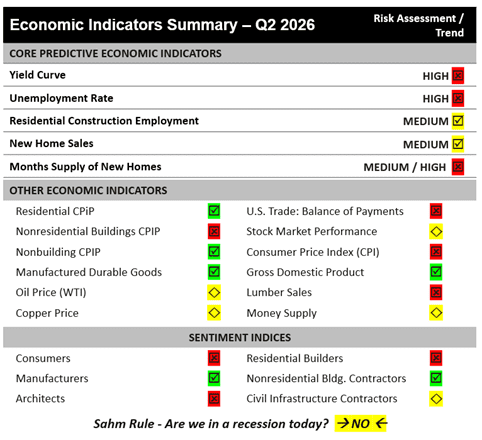

Three of five core predictive measures are still flashing warning signals. The yield curve leads those concerns, along with an unemployment rate that has trended higher over the past year, reaching 4.3% in April.

Housing carries most of the near-term risk. Inventory is high, and residential construction employment has fallen year over year for 13 straight months. Markets have also flipped from anticipating rate cuts to bracing for possible hikes. On June 17, the Federal Reserve held the federal funds rate at 3.5% to 3.75%. In its statement on the decision, Fed officials stressed the challenges posed by elevated inflation, driven in part by energy supply shocks, while pledging to deliver price stability.

Fed projections raised the 2026 inflation outlook to 3.6% and lifted the median year-end rate to 3.8%. Officials now forecast that inflation will not fall back to 2% until 2028. For rate-sensitive work, that points to higher borrowing costs for longer, with little near-term relief.

Backlogs Tell a Different Story

Despite those warning signs, contractor sentiment has improved in recent months. That improvement shows up most clearly in backlogs.

FMI’s Nonresidential Construction Index rose to 55.1 in the third quarter, up from 53.4. Contractors’ expectations for their own businesses climbed to 70.7, and backlog readings improved to 69.8. The Civil Infrastructure Construction Index recovered to 52.3 from 50.1, moving back above the neutral line. Its backlog measure strengthened, and its book-to-burn rate jumped to 57.4.

The largest firms tell a similar story, even as they grow more cautious about the national economy. In FMI’s latest Construction Industry Round Table Sentiment Index — a survey of leading design and construction CEOs — the backlog reading rose to 75.5. Nearly 60% of members expect backlogs to grow further next quarter.

This gap illustrates that funded, contracted work is carrying sentiment. Data centers are the strongest segment in this quarter’s Round Table survey, with industrial, transportation and public infrastructure close behind. Rate-sensitive sectors like office, lodging and commercial remain the softest.

Costs Remain a Shared Concern

Cost pressure is a concern across every panel. NRCI and CICI input readings fell well below 50, a sign that contractors expect costs to keep climbing. Ninety percent of Round Table members expect input costs to rise next quarter. Based on information to date, FMI expects construction-cost inflation to run between 5% and 7%, or higher, this year.

Cost pressures look broad. Building-material prices are climbing at their fastest pace in three years, even though oil remains the main swing factor behind the headline CPI of 4.2%. Energy costs work into diesel, freight and asphalt on a lag, so cost pressure can persist even after crude oil prices fall.

What This Means for Precast Producers

For precast producers, durable demand still sits in the segments least exposed to interest rates. FMI projects strong, stable investment across infrastructure segments including data centers (AI and digital infrastructure), power and transportation. Each is supported by committed funding, regulatory drivers or contracted load growth, so backlog growth rests on real work rather than sentiment alone. On federal-aid highway and transportation work, the Federal Highway Administration’s tightening of domestic content rules adds another advantage for domestic producers.

The practical takeaway: treat the backlog as an opportunity, and treat the cost outlook as a risk to manage. Capacity aligned with funded infrastructure, power and data center work offers the steadiest demand into 2027 and over the next several years. Bid and escalation terms should reflect a pricing environment that nearly every contractor expects to worsen.

Source: FMI’s quarterly indices, including the Q3 2026 Nonresidential Construction Index, Civil Infrastructure Construction Index and the latest Construction Industry Round Table Sentiment Index, are available at fmicorp.com/insights/indices. Read the full forecast in the FMI North American Engineering and Construction Outlook, with the third quarter edition arriving in July.

Brian Strawberry, a chief economist in the construction industry, leads FMI’s efforts in market sizing, forecasting, building products and construction material pricing, and consumption trends. He focuses on primary research methods, including the implementation and analysis of surveys and interviews. Brian also leads and manages various external market research engagements and constructs tools and models for efficiently performing high-quality analyses.